Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

1. Introduction

The concept of convergence analysis is an essential part of any numerical method. Binomial trees, for instance, are a popular numerical method used in finance to price options. However, the accuracy and efficiency of binomial trees depend on their convergence properties. This section will provide an overview of convergence analysis and its importance in assessing the accuracy and efficiency of binomial trees.

1. What is convergence analysis?

Convergence analysis is the process of determining whether a numerical method converges to the correct solution as the grid size or time step approaches zero. In other words, it refers to the rate at which a numerical method approaches the exact solution as the number of grid points or time steps increases. Convergence analysis is crucial since it helps ensure that the numerical method provides accurate results.

2. Why is convergence analysis important in binomial trees?

Binomial trees are discrete-time models that approximate the continuous-time behavior of options. They rely on the assumption that as the number of time steps increases, the option price converges to its true value. Therefore, it is essential to assess the convergence properties of binomial trees to determine their accuracy and efficiency in pricing options.

3. How is convergence analysis performed in binomial trees?

There are several methods for conducting convergence analysis in binomial trees. One approach is to compare the option price obtained from a binomial tree with the exact solution. This is done by using the Black-Scholes formula for European options or Monte Carlo simulation for more complex options. Another method is to calculate the convergence rate of the option price as the number of time steps increases. The convergence rate is usually estimated using regression analysis.

4. What are the factors that affect convergence in binomial trees?

Several factors can affect the convergence of binomial trees, including the number of time steps, the size of the time step, the volatility of the underlying asset, and the interest rate. Generally, as the number of time steps increases, the accuracy of the option price improves. However, increasing the number of time steps also increases the computational time required to price the option.

5. What are the alternatives to binomial trees for option pricing?

While binomial trees are a popular method for option pricing, there are alternative numerical methods that can be used, such as monte Carlo simulation, finite difference methods, and partial differential equations. monte Carlo simulation is a stochastic method that simulates the underlying asset's price path to estimate the option price. Finite difference methods and partial differential equations are continuous-time models that discretize the option pricing problem. Each method has its pros and cons, and the choice of method depends on the specific problem at hand.

Convergence analysis is a critical component of assessing the accuracy and efficiency of binomial trees in option pricing. It involves determining the rate at which the numerical method approaches the exact solution as the grid size or time step approaches zero. Several factors can affect the convergence of binomial trees, and there are alternative numerical methods that can be used for option pricing. Ultimately, the choice of method depends on the specific problem and the trade-off between accuracy and computational time.

Introduction - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

2. Overview of Binomial Trees

Binomial trees are a popular method for pricing options and other financial derivatives. They are a type of numerical method that involves discretizing the time and space dimensions of the underlying asset price process. The basic idea is to create a tree-like structure where each node represents a possible price of the underlying asset at a particular time. By recursively calculating the option value at each node, we can determine the option price at the initial time.

1. The Binomial Model

The binomial model is a simple example of a binomial tree. It assumes that the underlying asset price can either go up or down in each time step. The probabilities of these two outcomes are given by the up and down factors, u and d, respectively. The option value at each node is then calculated by taking the expected value of the future payoff, discounted back to the present time.

2. The cox-Ross-Rubinstein model

The Cox-Ross-Rubinstein (CRR) model is a more sophisticated version of the binomial model. It introduces a condition that ensures the model is arbitrage-free. This condition is known as the "no-arbitrage" condition and it ensures that the option price is consistent with the underlying asset price. The CRR model also introduces a parameter called the risk-neutral probability, which is used to calculate the expected future payoff.

3. Advantages and Disadvantages of Binomial Trees

One advantage of binomial trees is that they are relatively easy to implement and understand. They can be used to price a wide range of options, including American options, which are difficult to price using other methods. Binomial trees are also flexible and can be adapted to handle more complex models, such as stochastic volatility models.

However, there are also some disadvantages to using binomial trees. One major disadvantage is that they can be computationally intensive, especially for large trees or complex models. They also require the user to make assumptions about the underlying asset price process, which can introduce errors into the pricing model.

4. Conclusion

Overall, binomial trees are a useful tool for pricing options and other financial derivatives. They offer a flexible and intuitive way to model the underlying asset price process and can be adapted to handle a wide range of models. However, they do have some limitations and may not always be the best choice for every situation. As with any numerical method, it is important to carefully consider the assumptions and limitations of the model before using it to make financial decisions.

Overview of Binomial Trees - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

3. Definition and Importance

When it comes to assessing the accuracy and efficiency of binomial trees, convergence analysis plays a crucial role. In simple terms, convergence analysis refers to the process of examining whether the results obtained from a numerical method converge to the true solution as the number of iterations increases. The importance of convergence analysis cannot be overstated, as it helps in determining whether the numerical method used is reliable and accurate.

1. Definition of Convergence Analysis

Convergence analysis involves examining the rate at which a numerical method approaches the true solution as the number of iterations increases. The aim is to determine whether the numerical method converges to the true solution or not. If the method converges, it means that the results obtained are reliable and accurate. On the other hand, if the method does not converge, it means that the results obtained are not reliable and accurate.

2. Importance of Convergence Analysis

Convergence analysis is important for several reasons. First, it helps in determining whether the numerical method used is reliable and accurate. If the method does not converge, it means that the results obtained are not reliable and accurate. Second, it helps in determining the rate at which the numerical method approaches the true solution. This information is crucial in determining the efficiency of the numerical method used. Finally, it helps in comparing different numerical methods to determine which one is the most reliable and accurate.

3. Types of Convergence Analysis

There are two types of convergence analysis: pointwise convergence and uniform convergence. Pointwise convergence refers to the convergence of the numerical method at each point in the domain. Uniform convergence, on the other hand, refers to the convergence of the numerical method over the entire domain. Uniform convergence is preferred over pointwise convergence because it provides a more accurate measure of the reliability and accuracy of the numerical method.

4. Examples of Convergence Analysis

Consider the function f(x) = x^2. To determine the convergence of the numerical method used to approximate f(x), we can compare the results obtained at different values of x to the true solution. If the numerical method converges to the true solution as the number of iterations increases, it means that the method is reliable and accurate. If the numerical method does not converge, it means that the results obtained are not reliable and accurate.

5. Best Option for Convergence Analysis

The best option for convergence analysis depends on the problem being solved. In general, uniform convergence is preferred over pointwise convergence because it provides a more accurate measure of the reliability and accuracy of the numerical method. Additionally, it is important to compare different numerical methods to determine which one is the most reliable and accurate.

Definition and Importance - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

4. Assessing Accuracy of Binomial Trees

In the world of finance, binomial trees are widely used as a tool for pricing options. They are particularly useful when dealing with options that have complex features, such as American options or options with multiple exercise dates. However, the accuracy of binomial trees can be a concern, especially when compared to other pricing models such as Black-scholes. In this section, we will explore how to assess the accuracy of binomial trees and how to improve their performance.

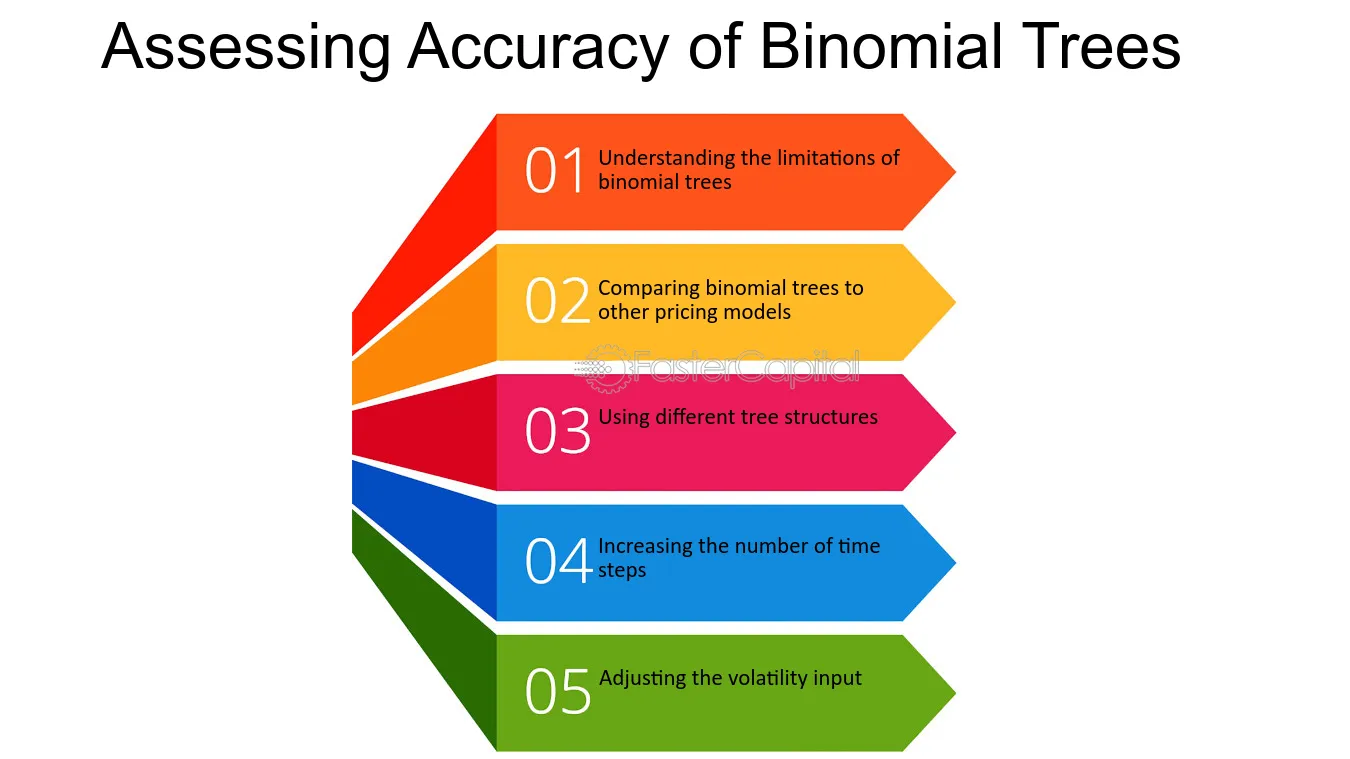

1. Understanding the limitations of binomial trees

Binomial trees are based on a number of assumptions, such as the assumption that the underlying asset follows a random walk and that the option can be exercised at discrete points in time. These assumptions can limit the accuracy of binomial trees, especially when dealing with options that have complex features. For example, if the underlying asset does not follow a random walk, the binomial tree may not accurately price the option. Similarly, if the option can be exercised at any time, the binomial tree may not capture the true value of the option.

2. comparing binomial trees to other pricing models

To assess the accuracy of binomial trees, it is important to compare them to other pricing models, such as Black-Scholes. Black-Scholes is a widely used pricing model that is based on the assumption that the underlying asset follows a log-normal distribution. While Black-Scholes is generally more accurate than binomial trees, it may not be suitable for all types of options. For example, Black-Scholes assumes that the option can only be exercised at expiration, which may not be true for all options.

3. Using different tree structures

Binomial trees can be constructed in a variety of ways, such as the Cox-Ross-Rubinstein (CRR) method or the Jarrow-Rudd method. Each method has its own strengths and weaknesses, and the choice of method can have an impact on the accuracy of the tree. For example, the CRR method is generally faster than the Jarrow-Rudd method, but may not be as accurate for options with complex features.

4. Increasing the number of time steps

One way to improve the accuracy of binomial trees is to increase the number of time steps used in the tree. This can be particularly effective for options with complex features or for options that have a long time to expiration. However, increasing the number of time steps can also increase the computational time required to price the option.

5. Adjusting the volatility input

Another way to improve the accuracy of binomial trees is to adjust the volatility input used in the tree. This can be done by using historical volatility data or by adjusting the implied volatility input. However, it is important to note that adjusting the volatility input can have a significant impact on the price of the option.

Assessing the accuracy of binomial trees is an important step in pricing options. By understanding the limitations of binomial trees, comparing them to other pricing models, using different tree structures, increasing the number of time steps, and adjusting the volatility input, we can improve the accuracy of binomial trees and ensure that they are an effective tool for pricing options.

Assessing Accuracy of Binomial Trees - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

5. Efficiency of Binomial Trees

In the world of finance, binomial trees are widely used to value derivatives. They are a popular method because they are relatively simple to understand and implement, and they can be used to value a wide range of financial instruments. However, one of the key concerns when using binomial trees is their efficiency. In this section, we explore the efficiency of binomial trees and how it affects their accuracy.

1. What is efficiency?

Efficiency is a measure of how well a method performs in terms of time and resources. In the context of binomial trees, efficiency refers to how quickly the tree can be generated and how much memory it requires. The more efficient a binomial tree is, the faster it can be used to value derivatives, and the less memory it requires.

2. How are binomial trees generated?

Binomial trees are generated by recursively calculating the value of the underlying asset at each node in the tree. This is done using the risk-neutral probability of the underlying asset moving up or down in price. The value of the derivative is then calculated at each node in the tree by working backwards from the final node.

3. What affects the efficiency of binomial trees?

There are several factors that can affect the efficiency of binomial trees:

- The number of time steps: The more time steps there are in the tree, the more nodes there are to calculate, which can make the tree slower and require more memory.

- The number of underlying asset price levels: The more price levels there are, the more nodes there are to calculate, which can make the tree slower and require more memory.

- The type of derivative being valued: Some derivatives require more time steps or price levels to accurately value, which can make the tree slower and require more memory.

4. What are some methods to improve the efficiency of binomial trees?

There are several methods that can be used to improve the efficiency of binomial trees:

- Truncating the tree: Truncating the tree by cutting off nodes that are unlikely to be reached can reduce the number of nodes that need to be calculated, which can make the tree faster and require less memory.

- Using a multiplicative binomial tree: A multiplicative binomial tree can be used instead of an additive binomial tree to reduce the number of time steps required to accurately value certain derivatives.

- Using a more efficient programming language: Using a more efficient programming language, such as C++ or Fortran, can make the tree faster and require less memory.

5. What is the best option for improving the efficiency of binomial trees?

The best option for improving the efficiency of binomial trees will depend on the specific situation. Truncating the tree can be a good option if there are many nodes that are unlikely to be reached. Using a multiplicative binomial tree can be a good option if the derivative being valued requires a large number of time steps. Using a more efficient programming language can be a good option if the tree is being used to value many derivatives. In general, it is important to balance accuracy and efficiency when using binomial trees to value derivatives.

Efficiency of Binomial Trees - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

6. Factors Affecting Convergence

When it comes to the accuracy and efficiency of binomial trees, convergence analysis plays a crucial role. Convergence refers to the process of a numerical method approaching a solution as the number of iterations increases. In the context of binomial trees, convergence analysis helps us determine the number of iterations required to achieve a desired level of accuracy. However, there are several factors that can affect the convergence of binomial trees. In this section, we will discuss some of the key factors affecting convergence.

1. Time Steps:

The number of time steps is a critical factor that affects convergence in binomial trees. In general, the more time steps we use, the more accurate our results will be. However, using too many time steps can also lead to slower convergence. Therefore, it is important to find the right balance between accuracy and efficiency. One way to achieve this is to use adaptive time steps, where the number of time steps is adjusted based on the level of accuracy required.

2. Volatility:

Volatility is another important factor that affects convergence in binomial trees. Higher volatility can lead to slower convergence, as it increases the complexity of the model. On the other hand, lower volatility can lead to faster convergence, but may also result in less accurate results. Therefore, it is important to choose the right level of volatility based on the specific requirements of the model.

3. Option Type:

The type of option being priced also affects convergence in binomial trees. For example, European options typically converge faster than American options, as they have a simpler payoff structure. On the other hand, exotic options with complex payoff structures may require more time steps to achieve a desired level of accuracy. Therefore, it is important to consider the type of option being priced when performing convergence analysis.

4. Interest Rates:

interest rates can also affect convergence in binomial trees. higher interest rates can lead to slower convergence, as they increase the complexity of the model. On the other hand, lower interest rates can lead to faster convergence, but may also result in less accurate results. Therefore, it is important to choose the right level of interest rates based on the specific requirements of the model.

5. Dividend Yield:

Dividend yield is another factor that can affect convergence in binomial trees. higher dividend yields can lead to slower convergence, as they increase the complexity of the model. On the other hand, lower dividend yields can lead to faster convergence, but may also result in less accurate results. Therefore, it is important to choose the right level of dividend yield based on the specific requirements of the model.

There are several factors that can affect convergence in binomial trees. It is important to consider these factors when performing convergence analysis, in order to achieve the right balance between accuracy and efficiency. By choosing the right time steps, volatility, option type, interest rates, and dividend yield, we can ensure that our binomial tree models are accurate and efficient.

Factors Affecting Convergence - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

7. Comparison with other Pricing Methods

When it comes to pricing financial instruments, there are different methods that can be used to calculate the value of the asset. Each method has its own strengths and weaknesses and can be applied to different types of assets. In this section, we will compare some of the most common pricing methods and evaluate their effectiveness in pricing options using binomial trees.

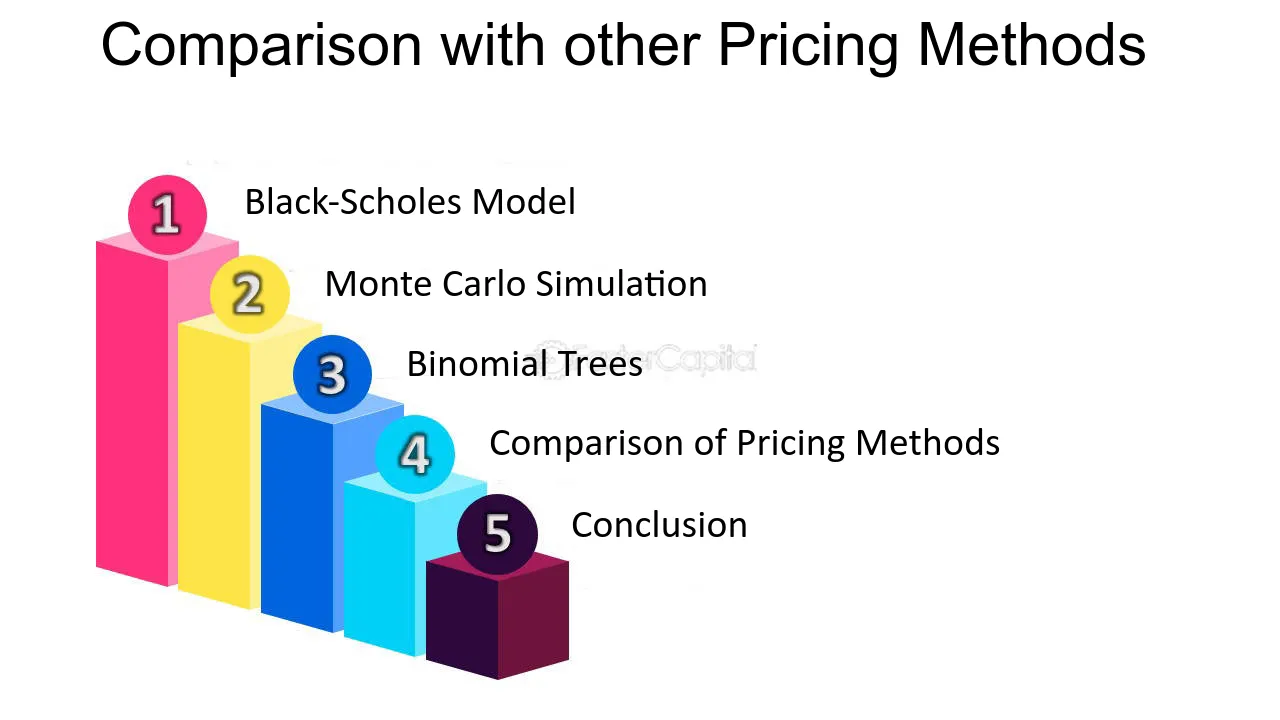

1. black-Scholes model

The Black-Scholes model is a widely used pricing method that assumes the underlying asset follows a lognormal distribution. It involves calculating the expected value of the asset using the risk-free rate, volatility, and time to maturity. While the model is widely used and has been successful in pricing many options, it has some limitations. The model assumes that the underlying asset follows a lognormal distribution, which may not always be the case. It also assumes that the market is always efficient, which may not be true in all cases.

2. Monte Carlo Simulation

Monte Carlo simulation is another pricing method that involves using random numbers to simulate the possible outcomes of an underlying asset. It involves simulating the asset price at different time points and calculating the expected value based on the simulated outcomes. Monte Carlo simulation is flexible and can be used to price a wide range of options. However, it can be computationally expensive and may not always provide accurate results.

3. Binomial Trees

Binomial trees are a popular pricing method for options that involve discrete time steps. The method involves constructing a tree of possible outcomes for the underlying asset and calculating the expected value at each node. Binomial trees are flexible and can be used to price a wide range of options, including those with early exercise features. They are also computationally efficient and can provide accurate results.

4. Comparison of Pricing Methods

When comparing pricing methods, it is important to consider the assumptions and limitations of each method. The Black-Scholes model is widely used and has been successful in pricing many options. However, it may not always be suitable for assets that do not follow a lognormal distribution or in markets that are not efficient. Monte Carlo simulation is flexible and can be used to price a wide range of options, but it can be computationally expensive and may not always provide accurate results. Binomial trees are flexible, computationally efficient, and can provide accurate results for a wide range of options.

5. Conclusion

There are different pricing methods that can be used to price financial instruments. Each method has its own strengths and weaknesses and can be applied to different types of assets. When choosing a pricing method, it is important to consider the assumptions and limitations of each method and choose the method that is most suitable for the asset being priced. In the case of pricing options using binomial trees, the binomial tree method is a flexible and computationally efficient method that can provide accurate results for a wide range of options.

Comparison with other Pricing Methods - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

8. Practical Applications of Convergence Analysis

Convergence analysis is a powerful tool that allows us to assess the accuracy and efficiency of binomial trees. It is widely used in finance, engineering, and other fields to determine the convergence rate of numerical methods and algorithms. In this section, we will explore some practical applications of convergence analysis and how it can be used to improve the accuracy and efficiency of numerical methods.

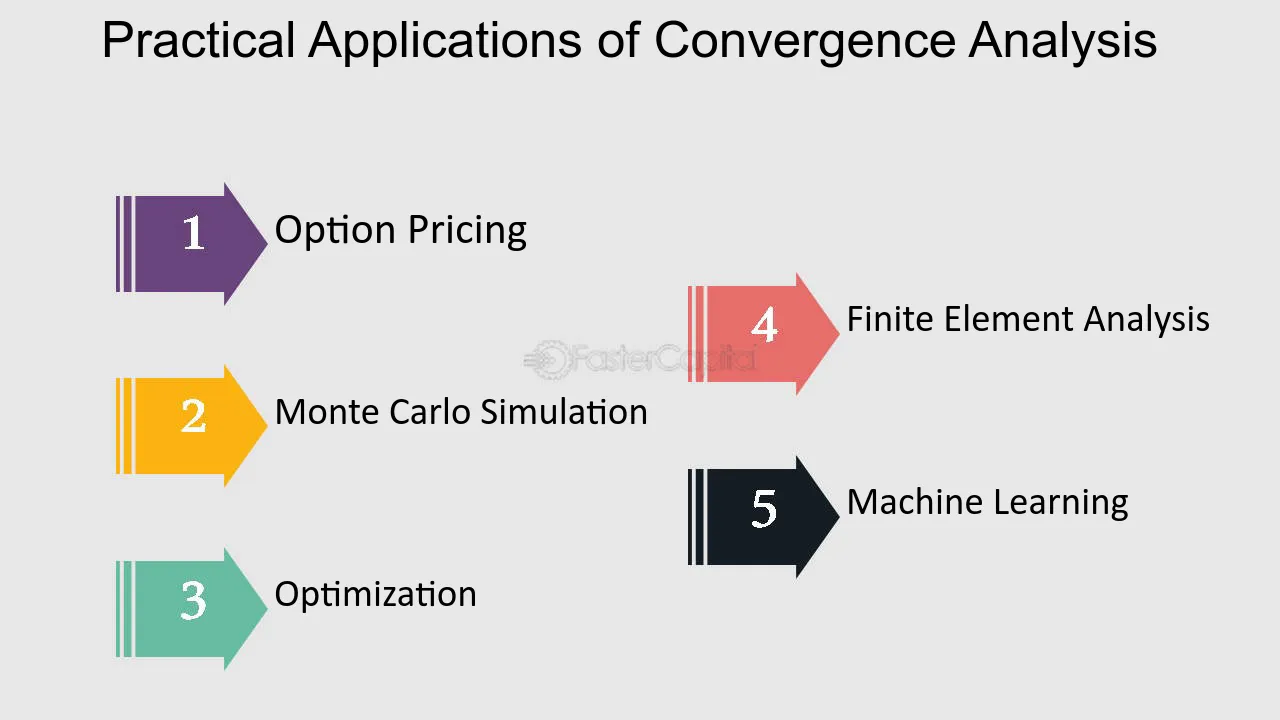

1. Option Pricing

One of the most important applications of convergence analysis is in option pricing. Binomial trees are commonly used to price options, and convergence analysis can help us determine the number of steps required to achieve a certain level of accuracy. For example, suppose we want to price an option with an accuracy of 0.01. Convergence analysis can tell us how many steps we need to take in the binomial tree to achieve this level of accuracy.

2. Monte Carlo Simulation

Convergence analysis is also useful in Monte Carlo simulation, which is a method for estimating the value of complex financial instruments. Monte Carlo simulation involves generating a large number of random samples and using them to estimate the value of the instrument. Convergence analysis can help us determine the number of samples required to achieve a certain level of accuracy. For example, if we want to estimate the value of an option with an accuracy of 0.01, convergence analysis can tell us how many samples we need to generate.

3. Optimization

Convergence analysis is also important in optimization, which involves finding the best solution to a problem. Many optimization algorithms use numerical methods, and convergence analysis can help us determine the convergence rate of these methods. This information can be used to improve the efficiency of the algorithm by choosing a method with a faster convergence rate.

Finite element analysis is a method for solving partial differential equations that arise in engineering and physics. Convergence analysis is essential in finite element analysis to ensure that the solution is accurate and reliable. Convergence analysis can help us determine the number of elements required to achieve a certain level of accuracy. This information can be used to optimize the mesh size and improve the efficiency of the analysis.

5. Machine Learning

Convergence analysis is also important in machine learning, which involves training models to make predictions based on data. Many machine learning algorithms use numerical methods, and convergence analysis can help us determine the convergence rate of these methods. This information can be used to choose an algorithm with a faster convergence rate and improve the efficiency of the training process.

Convergence analysis is a powerful tool that has many practical applications in finance, engineering, and other fields. It allows us to assess the accuracy and efficiency of numerical methods and algorithms and optimize them for better performance. By understanding the practical applications of convergence analysis, we can improve our ability to solve complex problems and make better decisions.

Practical Applications of Convergence Analysis - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees

9. Conclusion and Future Directions

After assessing the accuracy and efficiency of binomial trees for option pricing, it is clear that this method is a valuable tool for financial analysts. However, as with any mathematical model, there are limitations and areas for improvement. In this section, we will discuss the conclusions we have drawn from our analysis and potential future directions for research.

1. Conclusions

- Binomial trees provide a reasonably accurate method for pricing european and American options. However, the accuracy is dependent on the number of time steps used in the model. Increasing the number of time steps can improve the accuracy but also increases the computational complexity.

- The efficiency of the model is dependent on the number of time steps used and the option's parameters. The computational time increases as the number of time steps increases, but the efficiency is also affected by the option's strike price, time to maturity, and volatility.

- The model's accuracy and efficiency can be further improved by incorporating stochastic volatility models or other advanced techniques.

- The choice of the tree structure also affects the accuracy and efficiency of the model. The Cox-Ross-Rubinstein (CRR) model is widely used, but other models such as the Jarrow-Rudd (JR) or Tian models may be more suitable for certain option types.

- The binomial tree model is a great alternative to the Black-Scholes model, especially when pricing American options, which cannot be priced analytically using the Black-Scholes formula.

2. Future Directions

- The binomial tree model can be extended to include more complex options such as exotic options, options with early exercise features, or options with path-dependent payoffs.

- The model can be further improved by incorporating jump-diffusion models or other advanced stochastic processes.

- The convergence of the model can be improved by using adaptive time-stepping methods or other numerical techniques.

- The model can be used for risk management purposes, such as calculating the Greeks or simulating the option's value under different market scenarios.

- The model can be extended to include other asset classes such as commodities, interest rates, or credit derivatives.

The binomial tree model is a valuable method for pricing options, but there is still room for improvement and expansion. Further research can lead to more accurate and efficient models that can be used for a wider range of options and asset classes.

Conclusion and Future Directions - Convergence analysis: Assessing Accuracy and Efficiency of Binomial Trees