An essay on substack; interpreting US inflation history via fiscal theory, prepared as comments for a session at the AEA meetings.

Showing posts with label Economists. Show all posts

Showing posts with label Economists. Show all posts

Thursday, January 4, 2024

Sunday, December 17, 2023

Bond risk premiums -- certainty found and lost again

This is a second post from a set of comments I gave at the NBER Asset Pricing conference in early November at Stanford. Conference agenda here. My full slides here. First post here, on new-Keynesian models

I commented on "Downward Nominal Rigidities and Bond Premia" by François Gourio and Phuong Ngo. The paper was about bond premiums. Commenting made me realize that I thought I understood the issue, and now I realize I don't at all. Understanding term premiums still seems a fruitful area of research after all these years.

I thought I understood risk premiums

The term premium question is, do you earn more money on average holding long term bonds or short-term bonds? Related, is the yield curve on average upward or downward sloping? Should an investor hold long or short term bonds?

Friday, December 8, 2023

New-Keynesian models, a puzzle of scientific sociology

This post is from a set of comments I gave at the NBER Asset Pricing conference in early November at Stanford. Conference agenda here. My full slides here. There was video, but sadly I took too long to write this post and the NBER took down the conference video.

I was asked to comment on "Downward Nominal Rigidities and Bond Premia" by François Gourio and Phuong Ngo. It's a very nice clean paper, so all I could think to do as discussant is praise it, then move on to bigger issues. These are really comments about whole literatures, not about one paper. One can admire the play but complain about the game.

The paper implements a version of Bob Lucas' 1973 "International evidence" observation. Prices are less sticky in high inflation countries. The Phillips curve more vertical. Output is less affected by inflation. The Calvo fairy visits every night in Argentina. To Lucas, high inflation comes with variable inflation, so people understand that price changes are mostly aggregate not relative prices, and ignore them. Gourio and Ngo use a new-Keynesian model with downwardly sticky prices and wages to express the idea. When inflation is low, we're more often in the more-sticky regime. They use this idea in a model of bond risk premia. Times of low inflation lead to more correlation of inflation and output, and so a different correlation of nominal bond returns with the discount factor, and a different term premium.

I made two points, first about bond premiums and second about new-Keynesian models. Only the latter for this post.

This paper, like hundreds before it, adds a few ingredients on top of a standard textbook new-Keynesian model. But that textbook model has deep structural problems. There are known ways to fix the problems. Yet we continually build on the standard model, rather than incorporate known ways or find new ways to fix its underlying problems.

Problem 1: The sign is "wrong" or at least unconventional.

Monday, December 4, 2023

FTPL news: discount and Economist list

Just in time for the holidays, the perfect stocking stuffer -- if you have really big stockings. 30% discount on Fiscal Theory of the Price Level until June 30 2024.

And Fiscal Theory makes the Economist's list of best books for 2023.

Friday, October 13, 2023

Heterogeneous Agent Fiscal Theory

Today, I'll add an entry to my occasional reviews of interesting academic papers. The paper: "Price Level and Inflation Dynamics in Heterogeneous Agent Economies," by Greg Kaplan, Georgios Nikolakoudis and Gianluca Violante.

One of the many reasons I am excited about this paper is that it unites fiscal theory of the price level with heterogeneous agent economics. And it shows how heterogeneity matters. There has been a lot of work on "heterogeneous agent new-Keynesian" models (HANK). This paper inaugurates heterogeneous agent fiscal theory models. Let's call them HAFT.

Monday, August 28, 2023

Interest rates and inflation part 3: Theory

This post takes up from two previous posts (part 1; part 2), asking just what do we (we economists) really know about how interest rates affect inflation. Today, what does contemporary economic theory say?

As you may recall, the standard story says that the Fed raises interest rates; inflation (and expected inflation) don't immediately jump up, so real interest rates rise; with some lag, higher real interest rates push down employment and output (IS); with some more lag, the softer economy leads to lower prices and wages (Phillips curve). So higher interest rates lower future inflation, albeit with "long and variable lags."

Higher interest rates -> (lag) lower output, employment -> (lag) lower inflation.

In part 1, we saw that it's not easy to see that story in the data. In part 2, we saw that half a century of formal empirical work also leaves that conclusion on very shaky ground.

As they say at the University of Chicago, "Well, so much for the real world, how does it work in theory?" That is an important question. We never really believe things we don't have a theory for, and for good reason. So, today, let's look at what modern theory has to say about this question. And they are not unrelated questions. Theory has been trying to replicate this story for decades.

The answer: Modern (anything post 1972) theory really does not support this idea. The standard new-Keynesian model does not produce anything like the standard story. Models that modify that simple model to achieve something like result of the standard story do so with a long list of complex ingredients. The new ingredients are not just sufficient, they are (apparently) necessary to produce the desired dynamic pattern. Even these models do not implement the verbal logic above. If the pattern that high interest rates lower inflation over a few years is true, it is by a completely different mechanism than the story tells.

I conclude that we don't have a simple economic model that produces the standard belief. ("Simple" and "economic" are important qualifiers.)

The simple new-Keynesian model

Thursday, August 10, 2023

Interest rates and inflation part 2: Losing faith in VARs

(This post continues part 1 which just looked at the data. Part 3 on theory is here)

When the Fed raises interest rates, how does inflation respond? Are there "long and variable lags" to inflation and output?

There is a standard story: The Fed raises interest rates; inflation is sticky so real interest rates (interest rate - inflation) rise; higher real interest rates lower output and employment; the softer economy pushes inflation down. Each of these is a lagged effect. But despite 40 years of effort, theory struggles to substantiate that story (next post), it's had to see in the data (last post), and the empirical work is ephemeral -- this post.

The vector autoregression and related local projection are today the standard empirical tools to address how monetary policy affects the economy, and have been since Chris Sims' great work in the 1970s. (See Larry Christiano's review.)

I am losing faith in the method and results. We need to find new ways to learn about the effects of monetary policy. This post expands on some thoughts on this topic in "Expectations and the Neutrality of Interest Rates," several of my papers from the 1990s* and excellent recent reviews from Valerie Ramey and Emi Nakamura and Jón Steinsson, who eloquently summarize the hard identification and computation troubles of contemporary empirical work.

Maybe popular wisdom is right, and economics just has to catch up. Perhaps we will. But a popular belief that does not have solid scientific theory and empirical backing, despite a 40 year effort for models and data that will provide the desired answer, must be a bit less trustworthy than one that does have such foundations. Practical people should consider that the Fed may be less powerful than traditionally thought, and that its interest rate policy has different effects than commonly thought. Whether and under what conditions high interest rates lower inflation, whether they do so with long and variable but nonetheless predictable and exploitable lags, is much less certain than you think.

Monday, August 7, 2023

Blinder, supply shocks, and nominal anchors

An a recent WSJ oped (which I will post here when 30 days have passed), I criticized the "supply shock" theory of our current inflation. Alan Blinder responds in WSJ letters

First, Mr. Cochrane claims, the supply-shock theory is about relative prices (that’s true), and that a rise in some relative price (e.g., energy) “can’t make the price of everything go up.” This is an old argument that monetarists started making a half-century ago, when the energy and food shocks struck. It has been debunked early and often. All that needs to happen is that when energy-related prices rise, many other prices, being sticky downward, don’t fall. That is what happened in the 1970s, 1980s and 2020s.

Second, Mr. Cochrane claims, the supply-shock theory “predicts that the price level, not the inflation rate, will return to where it came from—that any inflation should be followed by a period of deflation.” No. Not unless the prices of the goods afflicted by supply shocks return to the status quo ante and persistent inflation doesn’t creep into other prices. Neither has happened in this episode.

When economists disagree about fairly basic propositions, there must be an unstated assumption about which they disagree. If we figure out what it is, we can think more productively about who is right.

I think the answer here is simple: To Blinder there is no "nominal anchor." In my analysis, there is. This is a question about which one can honorably disagree. (WSJ opeds have a hard word limit, so I did not have room for nuance on this issue.)

Sunday, August 6, 2023

Rangvid on housing inflation

(This post is an interlude between history and VARs)

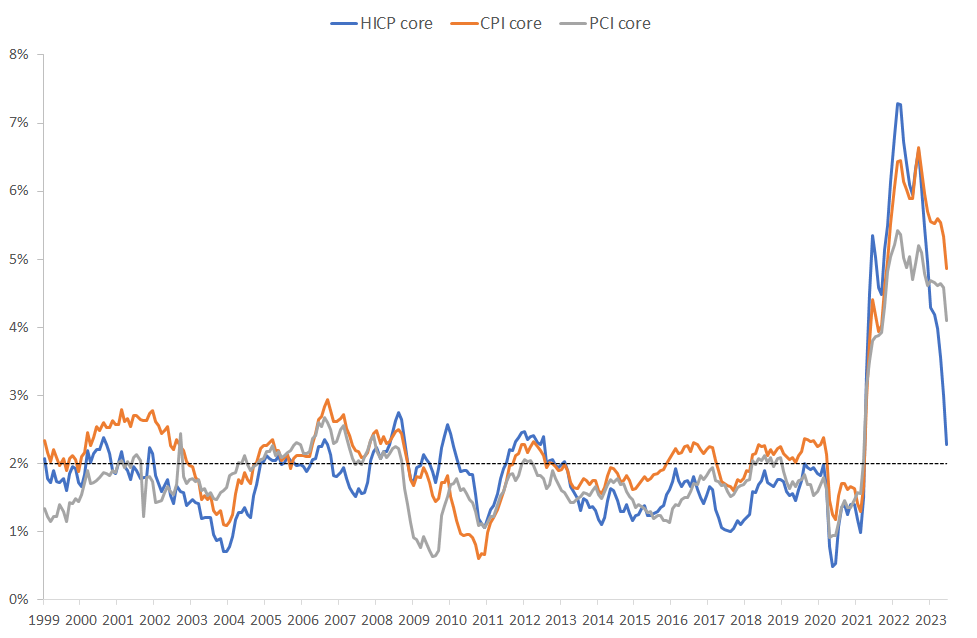

Jesper Rangvid has a great blog post today on different inflation measures.

CPI and PCE core inflation (orange and gray) are how the US calculates inflation less food and energy, but including housing. We do an economically sophisticated measure that tries to measure the "cost of housing" by rents for those who rent, plus how much a homeowner pays by "renting" the house to him or herself. You can quickly come up with the plus and minus of that approach, especially for looking at month to month trends in inflation. Europe in the "HICP core" line doesn't even try and leaves owner occupied housing out altogether.

Jesper's point: if you measure inflation Europe's way, US inflation is already back to 2%. The Fed can hang out a "mission accomplished" banner. (Or, in my view, a "it went away before we really had to do anything serious about it" banner.) And, since he writes to a European audience, Europe has a long way to go.

A few deeper (and slightly grumpier) points:

Tuesday, July 11, 2023

New York Times on HANK, and questions

By the standards of mainstream media coverage of technical economics, Peter Coy's coverage of HANK (Heterogeneous Agent New Keynesian) models in the New York Times was actually pretty good.

1) Representative agents and distributions.

Yes, it starts with the usual misunderstanding about "representative agents," that models assume we are all the same. Some of this is the standard journalist's response to all economic models: we have simplified the assumptions, we need more general assumptions. They don't understand that the genius of economic theory lies precisely in finding simplified but tractable assumptions that tell the main story. Progress never comes from putting more ingredients and stirring the pot to see what comes out. (I mean you, third year graduate students looking for a thesis topic.)

But in this case many economists are also confused on this issue. I've been to quite a few HANK seminars in which prominent academics waste 10 minutes or so dumping on the "assumption that everyone is identical."

There is a beautiful old theorem, called the "social welfare function." (I learned this in graduate school in fall 1979, from Hal Varian's excellent textbook.) People can have almost arbitrarily different preferences (utility functions), incomes and shocks, companies can have almost arbitrarily different characteristics (production functions), yet the aggregate economy behaves as if there is a single representative consumer and representative firm. The equilibrium path of aggregate consumption, output, investment, employment, and the prices and interest rates of that equilibrium are the same as those of an economy where everyone and every firm is the same, with a "representative agent" consumption function and "representative firm" production function. Moreover, the representative agent utility function and representative firm production function need not look anything like those of any particular individual person and firm. If I have power utility and you have quadratic utility, the economy behaves as if there is a single consumer with something in between.

Defining the job of macroeconomics to understand the movement over time of aggregates -- how do GDP, consumption, investment, employment, price level, interest rates, stock prices etc. move over time, and how do policies affect those movements -- macroeconomics can ignore microeconomics. (We'll get back to that definition in a moment.)

Monday, July 10, 2023

Inflation and debt across countries

Peder Beck-Friis and Richard Clarida at Pimco have a nice blog post on the recent inflation, including the above graph. I have wondered, and been asked, if the differences across countries in inflation lines up with the size of the covid fiscal expansion. Apparently yes.

Sunday, June 18, 2023

The perennial fantasy

Two attacks, and one defense, of classical liberal ideas appeared over the weekend. "War and Pandemic Highlight Shortcomings of the Free-Market Consensus" announces Patricia Cohen on p.1 of the New York Times news section. As if the Times had ever been part of such a "consensus." And Deirdre McCloskey reviews Simon Johnson and Daron Acemoglu's "Power and Progress," whose central argument is, per Deirdre, "The state, they argue, can do a better job than the market of selecting technologies and making investments to implement them." (I have not yet read the book. This is a review of the review only.)

I'll give away the punchline. The case for free markets never was their perfection. The case for free markets always was centuries of experience with the failures of the only alternative, state control. Free markets are, as the saying goes, the worst system; except for all the others.

In this sense the classic teaching of economics does a disservice. We start with the theorem that free competitive markets can equal -- only equal -- the allocation of an omniscient benevolent planner. But then from week 2 on we study market imperfections -- externalities, increasing returns, asymmetric information -- under which markets are imperfect, and the hypothetical planner can do better. Regulate, it follows. Except econ 101 spends zero time on our extensive experience with just how well -- how badly -- actual planners and regulators do. That messy experience underlies our prosperity, and prospects for its continuance.

Starting with Ms. Cohen at the Times,

The economic conventions that policymakers had relied on since the Berlin Wall fell more than 30 years ago — the unfailing superiority of open markets, liberalized trade and maximum efficiency — look to be running off the rails.

During the Covid-19 pandemic, the ceaseless drive to integrate the global economy and reduce costs left health care workers without face masks and medical gloves, carmakers without semiconductors, sawmills without lumber and sneaker buyers without Nikes.

That there ever was a "consensus" in favor of "the unfailing superiority of open markets, liberalized trade and maximum efficiency" seems a mighty strange memory. But if the Times wants to think now that's what they thought then, I'm happy to rewrite a little history.

Face masks? The face mask snafu in the pandemic is now, in the Times' rather hilarious memory, the prime example of how a free and unfettered market fails. It was a result of "the ceaseless drive to integrate the global economy and reduce costs?"

Tuesday, June 13, 2023

The barn door

Kevin Warsh has a nice WSJ oped warning of financial problems to come. The major point of this essay: "countercyclical capital buffers" are another bright regulatory idea of the 2010s that now has fallen flat.

As in previous posts, a lot of banks have lost asset value equal or greater than their entire equity due to plain vanilla interest rate risk. The ones that haven't run are now staying afloat only because you and me keep our deposits there at ridiculously low interest rates. Commercial real estate may be next. Perhaps I'm over-influenced by the zombie-apocalypse goings on in San Francisco -- $755 million default on the Hilton and Parc 55, $558 million default on the whole Westfield mall after Nordstrom departed and on and on. How much of this debt is parked in regional banks? I would have assumed that the Fed's regulatory army could see something so obvious coming, but since they completely missed plain vanilla interest rate risk, and the fact that you don't have to stand in line any more to run on your bank, who knows?

So, banks are at risk; the Fed now knows it, and is reportedly worried that more interest rates to lower inflation will cause more problems. To some extent that's a feature not a bug -- the whole theory behind the Fed lowering inflation is that higher interest rates "cool economic activity," i.e. make banks hesitant to lend, people lose their jobs, and through the Phillips curve (?) inflation comes down. But the Fed wants a minor contraction, not full-on 2008. (That did bring inflation down though!)

I don't agree with all of Kevin's essay, but I always cherry pick wisdom where I find it, and there is plenty. On what to do:

Ms. Yellen and the other policy makers on the Financial Stability Oversight Council should take immediate action to mitigate these risks. They should promote the private recapitalization of small and midsize banks so they survive and thrive.

Yes! But. I'm a capital hawk -- my answer is always "more." But we shouldn't be here in the first place.

Monday, June 12, 2023

Papers: Dew-Becker on Networks

I've been reading a lot of macro lately. In part, I'm just catching up from a few years of book writing. In part, I want to understand inflation dynamics, the quest set forth in "expectations and the neutrality of interest rates," and an obvious next step in the fiscal theory program. Perhaps blog readers might find interesting some summaries of recent papers, when there is a great idea that can be summarized without a huge amount of math. So, I start a series on cool papers I'm reading.

Today: "Tail risk in production networks" by Ian Dew-Becker, a beautiful paper. A "production network" approach recognizes that each firm buys from others, and models this interconnection. It's a hot topic for lots of reasons, below. I'm interested because prices cascading through production networks might induce a better model of inflation dynamics.

(This post uses Mathjax equations. If you're seeing garbage like [\alpha = \beta] then come back to the source here.)

To Ian's paper: Each firm uses other firms' outputs as inputs. Now, hit the economy with a vector of productivity shocks. Some firms get more productive, some get less productive. The more productive ones will expand and lower prices, but that changes everyone's input prices too. Where does it all settle down? This is the fun question of network economics.

Ian's central idea: The problem simplifies a lot for large shocks. Usually when problems are complicated we look at first or second order approximations, i.e. for small shocks, obtaining linear or quadratic ("simple") approximations.

Why? Because for large enough shocks, all the networky stuff disappears. Each firm's output moves up or down depending only on one critical input.

Thursday, June 8, 2023

Cost Benefit Comments

The Biden Administration is proposing major changes to cost-benefit analysis used in all regulations. The preamble here, and the full text here. It is open for public comments until June 20.

Economists don't often comment on proposed regulations. We should do so more often. Agencies take such comments seriously. And they can have an afterlife. I have seen comments cited in litigation and by judicial decisions. Even if you doubt the Biden Administration's desire to hear you on cost-benefit analysis, a comment is a marker that the inevitable eventual Supreme Court case might well consider. Comments tend only to come from interested parties and lawyers. Regular economists really should comment more often. I don't do it enough either.

You can see existing comments: Search for Circular A-4 updates to get to https://www.regulations.gov/docket/OMB-2022-0014, then select “browse all comments.” (Thanks to a good friend who sent this tip.)

Take a look at comments from an MIT team led by Deborah Lucas here and by Josh Rauh. These are great models of comments. You don't have to review everything. Make one good point.

Cost benefit analysis is useful even if imprecise. Lots of bright ideas in Washington (and Sacramento!) would struggle to document any net benefits at all. Yes, these exercises can lie, cheat, and steal, but having to come up with a quantitative lie can lay bare just how hare-brained many regulations are.

Wednesday, May 24, 2023

Hoover Monetary Policy Conference Videos

The videos from the Hoover Monetary Policy Conference are now online here. See my previous post for a summary of the conference.

The big picture is now clearer to me. Phil Jefferson rightly asked, what do you mean off track? Monetary policy is doing fine. Interest rates are, in his view, where they should be. He argued the case well.

But now I have an answer: The Fed has had three significant institutional failures: 1) Its inflation target is 2%, yet inflation exploded to 8%. The Fed did not forecast it, and did not see it even as it was happening. (Nor did many other forecasters, pointing to deeper conceptual problems.) 2) In the SVB and subsequent mess, the Fed's regulatory apparatus did not see or do anything about plain vanilla interest-rate risk combined with uninsured deposits. 3) I add a third, that nobody else seems to complain about: In 2020 starting with treasury markets, moving on to money market funds, state and local financing, and then an astonishing "whatever it takes" that corporate bond prices shall not fall, the Fed already revealed that the Dodd-Frank machinery was broken. (Will commercial real estate be next?)

Yet there is very little appetite for self-examination or even external examination. How did a good institution, filled with good, honest, smart and devoted public servants fail so badly? That's not "off-track" that's a derailment.

Well, two sessions at the conference begin to ask those questions, and the others aimed at the same issues. Hopefully they will prod the Fed to do so as well, or at least to be interested in other's answers to those questions.

(My minor contributions: on why the Taylor rule is important here, where I think I did a pretty good job; and comments on why inflation forecasts went so wrong at 1:00:16 here.)

Bradley Prize speech, video, and thanks

The videos and speeches of the Bradley prize winners are up. My video here (Grumpy in a tux!), also the speech which I reproduce below. All the videos and speeches here (Betsy DeVos and Nina Shea) My previous interview with Rick Graeber, head of the Bradley foundation.

Bradley also made a nice introduction video with photos from my childhood and early career. (A link here to the introduction video and speech together.) And to avoid us spending all our talks on thanking people, they had us write out a separate thanks. That seems not to be up yet, but I include mine below. I am very thankful, humbled to be included in such august company, and not so boorish that I would not have spent my whole talk without mentioning that, absent the separate opportunity to say so.

Bradley prize remarks (i.e. condense three decades of policy writing into 10 minutes):

Creeping stagnation ought to be recognized as the central economic issue of our time. Economic growth since 2000 has fallen almost by half compared with the last half of the 20th Century. The average American’s income is already a quarter less than under the previous trend. If this trend continues, lost growth in fifty years will total three times today’s economy. No economic issue — inflation, recession, trade, climate, income diversity — comes close to such numbers.

Growth is not just more stuff, it’s vastly better goods and services; it’s health, environment, education, and culture; it’s defense, social programs, and repaying government debt.

Why are we stagnating? In my view, the answer is simple: America has the people, the ideas, and the investment capital to grow. We just can’t get the permits. We are a great Gulliver, tied down by miles of Lilliputian red tape.

Wednesday, May 17, 2023

Bob Lucas and his papers

My first post described a few anecdotes about what a warm person Bob Lucas was, and such a great colleague. Here I describe a little bit of his intellectual influence, in a form that is I hope accessible to average people.

The “rational expectations” revolution that brought down Keynesianism in the 1970s was really much larger than that. It was really the “general equilibrium” revolution.

Macroeconomics until 1970 was sharply different from regular microeconomics. Economics is all about “models,” complete toy economies that we construct via equations and in computer programs. You can’t keep track of everything in even the most beautiful prose. Microeconomic models, and “general equilibrium” as that term was used at the time, wrote down how people behave — how they decide what to buy, how hard to work, whether to save, etc.. Then it similarly described how companies behave and how government behaves. Set this in motion and see where it all settles down; what prices and quantities result.

Tuesday, May 16, 2023

Hoover Monetary Policy Conference

Friday May 12 we had the annual Hoover monetary policy conference. Hoover twitter stream here. Conference webpage and schedule here (update 5/24 now contains videos.) As before, the talks, panels, and comments will eventually be written and published.

The Fed has experienced two dramatic institutional failures: Inflation peaking at 8%, and a rash of bank failures. There were panels focused on each, and much surrounding discussion.

Monday, May 15, 2023

Bob Lucas

I just got the sad news that Bob Lucas has passed away. He was truly a giant among economists, and a wonderful warm person.

I will only pass on three remembrances that others will not likely mention.

Bob was incredibly welcoming to me, a young brash and fairly untutored young economist from Berkeley.

In the fall of 1985 I gave what was no doubt the most disastrous first seminar by a new assistant professor in the Department's history. It was something about random walks and real business cycles, and was going nowhere. Bob stopped by my office, and expressed doubt about this random walk stuff. He said, if you look at longer and longer horizons, GNP volatility goes down. At least I had the wit to recognize what had just been handed to me on a silver platter, dropped everything and wrote the "Random walk in GNP," my first big paper. Without that, I doubt I would be where I am today. Thank you Bob. He and Nancy were kind to us socially as well.

The first Lucas paper that I recall reading, while I was still at Berkeley, was his review of a report to the OECD. I don't think anyone else writing about Bob will mention this masterpiece. If you get annoyed by policy blather, read this article. Reading it as a grad student, I loved the way he sliced through loose prose like warm butter. No BS with Bob. Only clear thinking please. I mentioned it later, and he laughed saying he wrote it in a bad mood because he was getting divorced. Like "After Keynesian Macroeconomics," Bob could wield a pen.

Much later, I attended a revelatory money workshop. Bob presented an early version of, I think, "Ideas and growth." In the model, people have ideas, and bump into each other randomly and share ideas. Questioner after questioner complained that there wasn't any economics in the model. Why not put in some incentive for people to bump in to each other, or something non mechanical. Time after time, Bob answered each suggestion that he had tried it, but it didn't make much difference to the outcome, so he stripped it out of the model. Clearly, he had been playing with this model over a year, working to eliminate needless ingredients, not to add more generality. It's great to see the production function at work.

Bob is known as a theorist, but he had a great handle on empirical work as well. His Carnegie Rochester money demand paper basically reinvented cointegration, and saw clearly what dozens of others missed. "Mechanics of economic development" starts by putting together facts. "International evidence on inflation-output tradeoffs" 1973 makes one stunning graph. And more.

There is so much to say about Bob the great economist, superb colleague and tremendous human being, but I will stop here for now. RIP Bob. And thank you.

Update:

Ben Moll has a lovely twitter thread about Bob as a thesis adviser. Bob covered Ben's thesis draft with useful comments. Bob read my early papers and did the same thing. This encouraged a culture of comments. Though a young assistant professor, I took it as a duty to write comments on Bob's papers! And some of them actually helped. This was the culture of the economics department in the 1980s, not common. Bob helped quite a few people and JPE authors to see what their papers were really about, making dramatic improvements.

The outpouring on twitter is remarkable. More remarkable, here is a man for whom we could celebrate every single paper as pathbreaking. Yet the outpouring is all about his wonderful personal qualities.

A correspondent reminds me of one last story. Bob's divorce agreement specified half of his Nobel prize, which he paid. Asked by a reporter if he had regrets, he answered "A deal's a deal."

Next post, focused on intellectual contributions.

Subscribe to:

Comments (Atom)