Corporate Sustainability - Social Accounting

Download as PPTX, PDF0 likes141 views

Social accounting is a method for companies to evaluate the social and environmental impact of their operations. It provides tools to collect, analyze, and monitor financial, social, and environmental data from both internal and external stakeholders. The goal is to demonstrate how companies are addressing issues like resource use, employee welfare, effects on the community, and their role as responsible corporate citizens. Social accounting measures can include expanded income statements, balance sheets, and schedules that account for social and environmental costs and benefits in both monetary and non-monetary terms. This allows companies to holistically evaluate and report on their social and economic contributions and impacts.

Corporate Sustainability - Social Accounting

- 2. Social Accounting – Why? What? Social accounting is a method by which a firm seeks to place a value on the impact on society of its operations. It is a systematic analysis of the effects of the organisation on its shareholders, with stakeholder input as part of the data that are analysed for the accounting statement. It provides tools and guidelines to collect, analyse and monitor financial, social and environment data. The concept of 'social accounting' relates to the manner in which an organisation interacts with its social surroundings. Many corporate, today, are providing information on their social performance in order to demonstrate to their shareholders and public that they are ethical and moral.

- 3. Social Accounting - Introduction There has been an explosion of interests in the company's social responsibilities in the recent years, and the phrase "being a responsible corporate citizen" has already become a core value. The very impact of the corporate sector in terms of finance and employment shows that the well- being of the corporate sector is of considerable significance to the society. In the environment of modern economic development, corporate sector no longer functions in isolation. The company must behave and function as a responsible member of the society just like any other individual. The real need is for some focus of accountability on the part of the management not being limited to shareholders alone but even the society. The acceptance of this concept of social responsibility must be reflected in the information and disclosure that the company makes available for the benefit of the various constituents like shareholders, creditors, workers and the community.

- 4. Social Accounting – Definition 1 • Kohler defined ‘social Accounting’ as the application of double entry book-keeping to socio-economic analysis.

- 5. Social Accounting – Definition 2 • Ralph Estes states Social accounting as the ‘measurement reporting, internal or external of information concerning the impact of an entity and its activities on society’.

- 6. Social Accounting – Definition 3 • In Sybil Mobley views ‘it refers to the ordering, measuring and analyses of the social and economic consequences of governmental and entrepreneurial behaviour’.

- 7. Social Accounting – Definition 4 • The National Association of Accountants (USA) defined it as the identification, measurement, monitoring and reporting of the social and economic effects of an institution on society.

- 8. Social Accounting – Definition 5 • Social Accounting is defined by Richard Dobbins and David Fanning as “the measurement and reporting of information concerning the impact of an entity and its activities on society”.

- 9. Social Accounting – Definition 6 • According to Ramanathan “Social Accounting is the process of selecting firm level social performance variables, measures and measurement procedures systematically developing information useful for evaluating performance and communicating such information to concerned social groups both within and outside the organisation.”

- 10. Social Accounting - Objectives The concept of social accounting gained prominence and momentum as a result of high level of industrialization that had necessitated the corporate to invest substantial amount in the social activities. Main objectives of social accounting are to help society by providing different facilities by enterprise and to record them like: 1. Effective utilization of natural resources Main objectives of making social accounting are to determine whether company is properly utilising their natural resources or not. To identify and measure the periodic net social contribution of an individual firm consisting of cost and benefits internalised to the firm and externalities affecting social system.

- 11. Social Accounting - Objectives 2. Help to employees Company can help employees by providing the facility of education to children of employees, providing transport free of cost and also providing good working environment conditions. 3. Help the society To help determine whether individual firms strategies and practices which directly affect the relative resource and power status of individuals, social segments, generations consistent with widely shared social priorities one hand and individual aspirations on the other. Because companies' factories spread the pollution in natural society which is very harmful for society .So, enterprise can help to society by planting the trees, establishing new parks near factory area and also opening new hospitals.

- 12. Social Accounting - Objectives 4. Help to customers If company provides goods to customers at lower rate and with high quality also benefits the society. To provide optimal information to all the constituents of the society to enable them to make decisions regarding allocation of the social resource where optimally implies cost/benefit effective reporting strategy which also optimally balances potential information conflicts among the various constituents of a firms.

- 13. Social Accounting - Objectives 5. Help to investors Company can help to investors by providing transparent accounting information to investors. Firms’ strategies and practices that directly affect relative resources can be determined. Because of many objectives are related to safeguarding of natural resources so this accounting is also known as Social and Environmental Accounting, Corporate Social Reporting, Corporate Social Responsibility Reporting, Non- Financial Reporting, Sustainability Accounting.

- 14. Social Accounting Measures • Undertakings through its annual reports publish the details of their social welfare and effect on society & workforce. (Sawalia B Verma: 1997)5

- 15. Social Accounting Measures – Cost Benefit Analysis 1 Social cost benefit analysis is a technique to weigh up the environmental and social benefits and costs of a business investment. 2 It is used to understand community expectations and concerns about the potential social and environmental impacts of a project to enable business to address these and make the project more acceptable. 3 Under this system the undertakings present social Balance Sheet and Social Income Statement. 4 The asset side of the balance sheet depict social investment of capital nature i.e Township, water supply, school, club, road etc. 5 The liability side shows organisations equity and social equations in the form of contribution by employees. 6 Social income statement comprises social benefit and cost of staff community and general public. 7 If social benefit exceeds social cost the resultant is not social income to staff, community and general public. (Boardman, Greenberg, Vining, Weimer: 2008)

- 16. Social Accounting Measures - Preparation of separate schedule • Schedules representing employees’ benefits and services, social overhead, township maintenance etc are prepared and shown as a part of annexure in the annual general report. • Employee benefits and services consist of salary and wages and various social security benefits. • Social overhead schedule include medical, educational, canteen and transportation facilities etc.

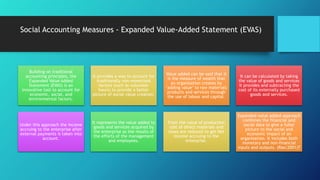

- 17. Social Accounting Measures - Expanded Value-Added Statement (EVAS) Building on traditional accounting principles, the Expanded Value Added Statement (EVAS) is an innovative tool to account for economic, social, and environmental factors. It provides a way to account for traditionally non-monetised factors (such as volunteer hours) to provide a better picture of social value creation. Value added can be said that it is the measure of wealth that an organisation creates by ‘adding value’ to raw materials products and services through the use of labour and capital. It can be calculated by taking the value of goods and services it provides and subtracting the cost of its externally purchased goods and services. Under this approach the income accruing to the enterprise after external payments is taken into account. It represents the value added to goods and services acquired by the enterprise as the results of the efforts of the management and employees. From the value of production cost of direct materials and taxes are reduced to get Net Income accruing to the enterprise. Expanded value added approach combines the financial and social data to give a fuller picture to the social and economic impact of an organisation. It includes both monetary and non-financial inputs and outputs. (Rao:2001)7

- 18. Social Accounting Measures – Other Approaches • Mention of social activities undertaken by an enterprise in chairman’s speech, directors’ report or auditor’s report. • This approach aims at informing the general public, government and its members about the organisations’ goals with economic goals. • Other method is pictorial presentation in annual report of social activities like sponsoring of social and charitable causes and other social welfare activities; supplementing of government efforts effectively; focusing on human elements; ensuring ecological balance, engaging in philanthropic activities undertaken in by the organisation.

- 19. The Need for Social Accounting • The practise of social accounting is followed only by a handful to enterprise in public sector. (Jahan:2001).That there is greater need for social accounting for; • The management fulfils its social obligations and informs its members, government and general public. • There are certain legal obligations that have to be fulfilled by the business, such as social security obligations and welfare measures etc. The management reforms the public and government about its efforts in this regard through social accounting. • Management gets a feedback on its efforts and policies aimed at welfare of the society. • Social accounting is also necessary from the viewpoint of public interest group, social organisation, investors and government bodies. • Through social accounting the company proves itself that it is not socially unethical in view of moral cultural and environment degradation.