![LECTURE 1 BASIC CONCEPTS OF ECONOMICS Shan Faculty of Business Management & Globalization Limkokwing Executive Leadership College [email_address] Tel: +603 - 8317 8833 (ext. 8407) BECON1201: Microeconomics MICROECONOMICS](https://image.slidesharecdn.com/lecture1-basiceconomicconcepts1-090930053723-phpapp01/85/Lecture1-Basic-Economic-Concepts-1-1-320.jpg)

![Economics as Social Science Need for integration of social sciences deductive, historical and empirical [statistical] approaches Philosophical and Historical Context To speculate about where you are going, you need to understand where you are To fully understand where you are, you need to know where you came from](https://image.slidesharecdn.com/lecture1-basiceconomicconcepts1-090930053723-phpapp01/85/Lecture1-Basic-Economic-Concepts-1-4-320.jpg)

![ECONOMIC SYSTEMS laissez-faire economy (free market) Literally from the French: “allow [them] to do.” An economy in which individual people and firms pursue their own self-interests without any central direction or regulation. market The institution through which buyers and sellers interact and engage in exchange. Some markets are simple and others are complex, but they all involve buyers and sellers engaging in exchange. The behavior of buyers and sellers in a laissez-faire economy determines what gets produced, how it is produced, and who gets it.](https://image.slidesharecdn.com/lecture1-basiceconomicconcepts1-090930053723-phpapp01/85/Lecture1-Basic-Economic-Concepts-1-28-320.jpg)

Lecture1 Basic Economic Concepts (1)

- 1. LECTURE 1 BASIC CONCEPTS OF ECONOMICS Shan Faculty of Business Management & Globalization Limkokwing Executive Leadership College [email_address] Tel: +603 - 8317 8833 (ext. 8407) BECON1201: Microeconomics MICROECONOMICS

- 2. Definition of Economics economics is a social science that studies human behavior and institutional arrangements in societies that influence the processes by which relatively scarce resources are allocated to alternative uses social science and decision science components of economics

- 3. Economics as a Social Science Human behavior is influenced by a matrix of complex forces Psychology Sociology Anthropology Economics Political Science Religion, ...

- 4. Economics as Social Science Need for integration of social sciences deductive, historical and empirical [statistical] approaches Philosophical and Historical Context To speculate about where you are going, you need to understand where you are To fully understand where you are, you need to know where you came from

- 5. Objectives The objective is the goal or desired outcome of a choice Individuals may try to maximize utility given the constraints of income, time, prices, etc. Firms may have objectives such as the maximization of profits, sales, market share, etc. or the minimization of costs per unit Social objective, maximize the well being of the members of society

- 6. WHAT IS ECONOMICS? scarcity The resources we use to produce goods and services are limited. economics The study of choices when there is scarcity. Here are some examples of scarcity and the trade-offs associated with making choices: • You have a limited amount of time. If you take a part-time job, each hour on the job means one less hour for study or play. • A city has a limited amount of land. If the city uses an acre of land for a park, it has one less acre for housing, retailers, or industry. • You have limited income this year. If you spend $17 on a music CD, that’s $17 less you have to spend on other products or to save.

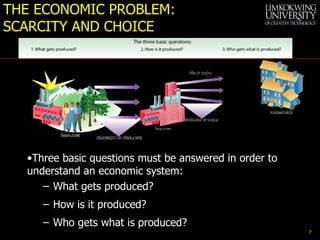

- 7. THE ECONOMIC PROBLEM: SCARCITY AND CHOICE Three basic questions must be answered in order to understand an economic system: What gets produced? How is it produced? Who gets what is produced?

- 8. WHAT IS ECONOMICS? F actors of production The resources used to produce goods and services; also known as production inputs. Natural resources/Land Resources provided by nature and used to produce goods and services. labour The physical and mental effort people use to produce goods and services. physical capital & Financial Capital The stock of equipment, machines, structures, and infrastructure that is used to produce goods and services. Input of funds human capital The knowledge and skills acquired by a worker through education and experience. entrepreneurship The effort used to coordinate the factors of production—natural resources, labor, physical capital, and human capital—to produce and sell products.

- 9. Resources Typical taxonomy land / natural resources labor Capital Entrepreneurial ability Alternative view Matter Energy Time Technology

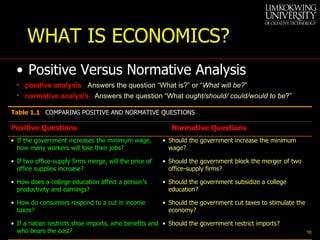

- 10. WHAT IS ECONOMICS? positive analysis Answers the question “What is?” or “ What will be? ” Positive Versus Normative Analysis normative analysis Answers the question “What ought/should/ could/would to be ?” Table 1.1 COMPARING POSITIVE AND NORMATIVE QUESTIONS Positive Questions Normative Questions • If the government increases the minimum wage, how many workers will lose their jobs? • Should the government increase the minimum wage? • If two office-supply firms merge, will the price of office supplies increase? • Should the government block the merger of two office-supply firms? • How does a college education affect a person’s productivity and earnings? • Should the government subsidize a college education? • How do consumers respond to a cut in income taxes? • Should the government cut taxes to stimulate the economy? • If a nation restricts shoe imports, who benefits and who bears the cost? • Should the government restrict imports?

- 11. THE ECONOMIC WAY OF THINKING Four elements of the economic way of thinking: 1 Use Assumptions to Simplify Economists use assumptions to make things simpler and focus attention on what really matters. 2 Isolate Variables— Ceteris Paribus Economic analysis often involves variables and how they affect one another. variable A measure of something that can take on different values. ceteris paribus The Latin expression meaning other variables being held fixed.

- 12. THE ECONOMIC WAY OF THINKING 3 Think at the Margin Economists often consider how a small change in one variable affects another variable and what impact that has on people’s decision making. marginal change A small, one-unit change in value. 4 Rational People Respond to Incentives A key assumption of most economic analysis is that people act rationally, meaning that they act in their own self-interest .

- 13. Building a Foundation: Economics and Individual Decisions Market : An arrangement or institution that brings together buyers and sellers of a good or service. Marginal analysis : Analysis that involves comparing marginal benefits and marginal costs. Three important ideas: People are rational People respond to economic incentives

- 14. Microeconomics and Macroeconomics Microeconomics The study of how households and businesses make choices, how they interact in markets, and how the government attempts to influence their choices. Macroeconomics The study of the economy as a whole, including topics such as inflation, unemployment, economic growth National income etc.

- 15. Nearly all the same basic decisions that characterize complex economies must also be made in a simple economy. SCARCITY, CHOICE, AND OPPORTUNITY COST SCARCITY AND CHOICE IN A ONE-PERSON ECONOMY

- 16. Scarcity Because of Scarcity, individuals and societies must make choices All Choices in a finite world have “opportunity costs” alternative uses of finite resources Opportunity cost is the value of the next best alternative sacrificed Can institutional structure create or increase scarcity?

- 17. The concepts of constrained choice and scarcity are central to the discipline of economics. SCARCITY, CHOICE, AND OPPORTUNITY COST opportunity costs The best alternative that we give up, or forgo, when we make a choice or decision.

- 18. SCARCITY, CHOICE, AND OPPORTUNITY COST Capital Goods and Consumer Goods consumer goods Goods produced for present consumption. investment The process of using resources to produce new capital. Because resources are scarce, the opportunity cost of every investment in capital is forgone present consumption.

- 19. SCARCITY, CHOICE, AND OPPORTUNITY COST production possibility frontier (ppf) A graph that shows all the combinations of goods and services that can be produced if all of society’s resources are used efficiently. THE PRODUCTION POSSIBILITY FRONTIER

- 20. SCARCITY, CHOICE, AND OPPORTUNITY COST FIGURE 2.3 Production Possibility Frontier

- 21. During economic downturns or recessions, industrial plants run at less than their total capacity. When there is unemployment of labor and capital, we are not producing all that we can. SCARCITY, CHOICE, AND OPPORTUNITY COST Unemployment

- 22. Waste and mismanagement are the results of a firm’s operating below its potential. Sometimes, inefficiency results from mismanagement of the economy instead of mismanagement of individual private firms. SCARCITY, CHOICE, AND OPPORTUNITY COST Inefficiency The Efficient Mix of Output To be efficient, an economy must produce what people want.

- 23. SCARCITY, CHOICE, AND OPPORTUNITY COST Negative Slope and Opportunity Cost FIGURE 2.4 Inefficiency from Misallocation of Land in Farming marginal rate of transformation (MRT) The slope of the production possibility frontier (ppf).

- 24. SCARCITY, CHOICE, AND OPPORTUNITY COST The Law of Increasing Opportunity Cost FIGURE 2.5 Corn and Wheat Production in Ohio and Kansas TABLE 2.1 Production Possibility Schedule for Total Corn and Wheat Production in Ohio and Kansas POINT ON PPF TOTAL CORN PRODUCTION (MILLIONS OF BUSHELS PER YEAR) TOTAL WHEAT PRODUCTION (MILLIONS OF BUSHELS PER YEAR) A 700 100 B 650 200 C 510 380 D 400 500 E 300 550

- 25. SCARCITY, CHOICE, AND OPPORTUNITY COST Economic Growth economic growth An increase in the total output of an economy. It occurs when a society acquires new resources or when it learns to produce more using existing resources.

- 26. SCARCITY, CHOICE, AND OPPORTUNITY COST FIGURE 2.6 Economic Growth Shifts the ppf Up and to the Right

- 27. SCARCITY, CHOICE, AND OPPORTUNITY COST THE ECONOMIC PROBLEM Recall the three basic questions facing all economic systems: (1) What gets produced? (2) How is it produced? (3) Who gets it? Given scarce resources, how exactly do large, complex societies go about answering the three basic economic questions?

- 28. ECONOMIC SYSTEMS laissez-faire economy (free market) Literally from the French: “allow [them] to do.” An economy in which individual people and firms pursue their own self-interests without any central direction or regulation. market The institution through which buyers and sellers interact and engage in exchange. Some markets are simple and others are complex, but they all involve buyers and sellers engaging in exchange. The behavior of buyers and sellers in a laissez-faire economy determines what gets produced, how it is produced, and who gets it.

- 29. ECONOMIC SYSTEMS Command economy An economy in which a central government either directly or indirectly sets output targets, incomes, and prices. Mixed economy is an economic system that incorporates a mixture of private and government ownership or control, or a mixture of capitalism and socialism

- 30. Goods and services Consumer expenditure Wages, rent dividends, etc. Services of factors of production (labour, etc) The circular flow of goods and incomes GOODS MARKETS FACTOR MARKETS