![ Step 2

Standard deviation

Risk of a portfolio expresses the extent to which the actual

return may deviate from the expected return.

Expressed by standard deviation or variance

𝜎p= [𝛼 2 𝜎𝐴2 +(1-𝛼)^2 𝜎𝐵^2 + 2𝛼(1 − 𝛼)𝑐𝑜𝑣𝐴𝐵]

Where;

𝛼 =the proportion of the portfolio invested in A

(1-𝛼) =proportion invested in B

𝜎𝐴2 = the variance of the return on asset A

𝜎𝐵2 = the variance of the return on asset B

cov AB=the covariance of the returns on A and B](https://image.slidesharecdn.com/portfoliomanagementlecture-140515063320-phpapp02/85/Portfolio-management-lecture-5-320.jpg)

![ Step 3

Covariance

A statistical measure of the extent to which the

fluctuations exhibited by two ore more variables are

related

Correlation coefficient is a measure of the

interrelationship between random variables

n

rAB= cov AB covAB= ∑ [pi(RA –ERA)(RB-ERB)]

𝜎A X 𝜎Bi=1](https://image.slidesharecdn.com/portfoliomanagementlecture-140515063320-phpapp02/85/Portfolio-management-lecture-6-320.jpg)

![Solution

Year Rb Rg db dg db2 dg2 db X dg

1 26.00% 24.00% 2.00% -6.00% 0.04% 0.36% -0.12%

2 20.00% 35.00% -4.00% 5.00% 0.16% 0.25% -0.20%

3 22.00% 22.00% -2.00% -8.00% 0.04% 0.64% 0.16%

4 23.00% 37.00% -1.00% 7.00% 0.01% 0.49% -0.07%

5 29.00% 32.00% 5.00% 2.00% 0.25% 0.04% 0.10%

0.50% 1.78% -0.13%

Average

return

24.00% 30.00%

Variance =db2/5 0.1 0.356

Std Dev. =var^0.5 0.316 0.597

Cov(bg) [db x dg]/5 -0.026%](https://image.slidesharecdn.com/portfoliomanagementlecture-140515063320-phpapp02/85/Portfolio-management-lecture-8-320.jpg)

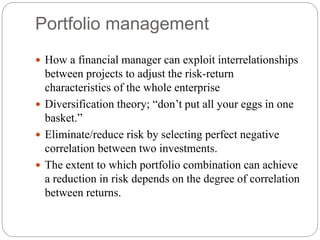

Portfolio management lecture

- 2. Portfolio management How a financial manager can exploit interrelationships between projects to adjust the risk-return characteristics of the whole enterprise Diversification theory; “don’t put all your eggs in one basket.” Eliminate/reduce risk by selecting perfect negative correlation between two investments. The extent to which portfolio combination can achieve a reduction in risk depends on the degree of correlation between returns.

- 3. Attitudes to risk Risk-averse – prefer less risk to more risk for a given return Moderately risk-averse Risk indifferent Investors would expect more return for increased risk

- 4. Two asset portfolio risk Step 1 Expected return The use of probability distribution on projected cash outcomes Given by the formula; n 𝑋 = ∑ piXi i=1 or ERp= 𝛼ERA + (1-𝛼)ERB

- 5. Step 2 Standard deviation Risk of a portfolio expresses the extent to which the actual return may deviate from the expected return. Expressed by standard deviation or variance 𝜎p= [𝛼 2 𝜎𝐴2 +(1-𝛼)^2 𝜎𝐵^2 + 2𝛼(1 − 𝛼)𝑐𝑜𝑣𝐴𝐵] Where; 𝛼 =the proportion of the portfolio invested in A (1-𝛼) =proportion invested in B 𝜎𝐴2 = the variance of the return on asset A 𝜎𝐵2 = the variance of the return on asset B cov AB=the covariance of the returns on A and B

- 6. Step 3 Covariance A statistical measure of the extent to which the fluctuations exhibited by two ore more variables are related Correlation coefficient is a measure of the interrelationship between random variables n rAB= cov AB covAB= ∑ [pi(RA –ERA)(RB-ERB)] 𝜎A X 𝜎Bi=1

- 7. Example Information is available for two shares; B Ltd and G Ltd. The returns of shareholders have been calculated for the last five years. Calculate the mean (expected return), standard deviation and covariance. Year B Ltd G Ltd 1 26% 24% 2 20% 35% 3 22% 22% 4 23% 37% 5 29% 32%

- 8. Solution Year Rb Rg db dg db2 dg2 db X dg 1 26.00% 24.00% 2.00% -6.00% 0.04% 0.36% -0.12% 2 20.00% 35.00% -4.00% 5.00% 0.16% 0.25% -0.20% 3 22.00% 22.00% -2.00% -8.00% 0.04% 0.64% 0.16% 4 23.00% 37.00% -1.00% 7.00% 0.01% 0.49% -0.07% 5 29.00% 32.00% 5.00% 2.00% 0.25% 0.04% 0.10% 0.50% 1.78% -0.13% Average return 24.00% 30.00% Variance =db2/5 0.1 0.356 Std Dev. =var^0.5 0.316 0.597 Cov(bg) [db x dg]/5 -0.026%

- 10. Line ABC represents a feasible set of portfolios of asset P and Q As expected investment return increases, the additional subjective satisfaction of an investor declines at an increasing rate Rate of decline is dependent upon the attitude toward risk of the individual investor

- 11. Benefits of diversification Reduces variability of portfolio returns Reduction in risk which comes with the increase in number of different shares in the portfolio Specific risk- unsystematic risk or diversifiable risk that is unique to a company Market risk-systematic risk or non-diversifiable risk e.g. changes in economic climate determined by inflation, interest rates and foreign exchange rates

- 12. Multiple-share portfolio risk and return