Building For A Billion

7 likes1,890 views

The document discusses the transformation brought about by platform models in the economy, emphasizing the shift from traditional producer-consumer value creation to interaction-driven value through digital platforms. It highlights India's digital infrastructure, particularly the India Stack system, which enables a presence-less, paperless, and cashless economy while enhancing financial inclusion. Additionally, it addresses the potential economic mobility and data empowerment for citizens through innovative technologies and consent-driven data sharing.

Building For A Billion

- 1. 1 Building For a Billion Nikhil Kumar, Fellow, iSPIRT Foundation @nikhilkumarks

- 2. Platform Model - Reimagining the creation of value 2 Old World - Pipes ● Producer creates value ● Deliver to customer New World - Platforms ● Interaction creates Value ● Network effects drive Scale Credit: Platform Scale - Sangeet Paul Choudary

- 3. Why Platforms Matter? ➔ Economic leverage has moved to platforms ➔ Social Impact

- 4. “A product is useless without a platform, or more precisely and accurately, a platform-less product will always be replaced by an equivalent platform-ized product.” Source: Steve Yegge’s rant on Google Platforms $360 billion $50 billion $366 billion Large Platforms… Evolve from leading digital products Steve Yegge

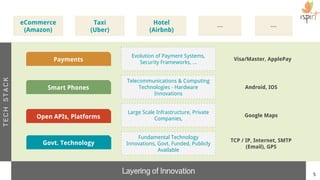

- 5. 5 TCP / IP, Internet, SMTP (Email), GPS Fundamental Technology Innovations, Govt. Funded, Publicly Available Payments Visa/Master, ApplePay Evolution of Payment Systems, Security Frameworks, ... Open APIs, Platforms Google Maps Large Scale Infrastructure, Private Companies, Smart Phones Android, IOS Telecommunications & Computing Technologies - Hardware Innovations TECHSTACK Layering of Innovation Govt. Technology eCommerce (Amazon) Taxi (Uber) Hotel (Airbnb) ------

- 6. Why Platforms Matter? ➔ Economic leverage has moved to platforms ➔ Social Impact

- 7. Platforms India Stack on JAM Made-in India Services Technology Platforms are the new leverage point India has a new soft power to leverage 1st Innings 2nd Innings Natural Resources Made-in-India Products Defense Aerospace Electronics Software Products 3rd Innings 4th Innings

- 8. India Stack

- 9. 9 Mobile Connections Aadhaar Enrolments Unique Bank Accounts Internet Users 1.21 Bn 1.19 Bn 582M 462M Social Media Users 375M India’s Digital Push

- 10. PRESENCE-LESS LAYER Aadhaar Authentication Unique digital biometric identity with open access of nearly a Billion users CONSENT LAYER National Policy on Data Sharing Provides a modern privacy data sharing framework PAPERLESS LAYER Aadhaar e-KYC, E-sign, Digital Locker Rapidly growing base of paperless systems with billions of artifacts CASHLESS LAYER IMPS, AEPS, APB, and UPI Game changing electronic payment systems and transition to cashless economy SUBSIDIES (DBT) COMMERCE (GST) BILLS (BBPS) OTHERS INDIASTACK TOLLS (ETC) JAM Jan Dhan, Aadhaar, Mobile India Stack

- 11. 11 Aadhaar Hourglass Architecture ❏ Identity as a utility, an enabler ❏ Allows innovation on all sides ❏ Amplifies ecosystem players Biometric Sensors Phones Tablets Attendance Device Micro ATM Healthcare Apps SIM Finance Apps UPI Digital Locker APB AEPS DBT eSign Aadhaar Applications / Systems Devices ● Minimal ● Standardized ● Simple design ● Easy to execute ● Easy to write a law

- 12. Name DoB/Age Gender Address Mobile/Email 1234 5678 9012 A Unique Lifetime Identity Aadhaar Authentication Aadhaar eKYC Are you who you claim to be? Paperlessly share KYC/AML details Aadhaar eSign Digitally Sign Documents

- 13. 10X number of Jandhan Bank Accounts in 3 years Starting with 30 Mn accounts in Sep-2014, India crossed 300 Mn Jandhan accounts in Sep-2017 Source: UIDAI website, PMJDY Website, as of Feb-2018 Aadhaar-Seeded Bank Accounts 850 Mn Unique Bank Account Holders 582 Mn

- 14. The usage is coming primarily from Govt, Banks & Telcos 10 BN Aadhaar Authentications In The Last Year There are now 5x as many Aadhaar Authentications daily (64 mn) than Card Transactions at PoS (12.7 Mn) Source: UIDAI website Monthly Cumulative Nandan Nilekani, 2018

- 15. 3.2 Billion eKYCs in 2017 Of the 3.86 Bn total eKYCs ever, only 0.4 Bn were before Dec ‘16 About a third of the usage is for Telecom. Other prominent use cases are for opening of financial services accounts Source: UIDAI website Monthly Cumulative

- 16. eSign - Digital signature for a billion Application Service Provider (ASP) 1.Online request for Digital Signature 2. Request for PoA/PoI Data 4. Online Instant Digital Signature Issued 3. PoA/PoI Through eKYC eSign Service Providers (ESP) UIDAI (for Aadhaar eKYC) Residents needing to sign a document Interoperable, Open API based, multi-provider, digital signing protocol, legally protected under IT Act 16Source: http://cca.gov.in

- 17. Digital Locker - eliminating fake papers Open API based Ecosystem driven Digitally protected Source: https://digilocker.gov.in Multi-provider Digital Locker EcosystemIssuer Requestor Users Issues Documents Digitally Accesses Documents Online Approves Access No Physical Papers No Fake Documents Nandan Nilekani, 2018

- 18. Registered Mobile Numbers Active Debit Cards Download UPI app & Transact 95+ Banks 600M Accounts Onboarding a billion a people at scale to Digital Payments

- 19. UPI doing more txns than Credit Cards In 18 Months! Source: RBI website Right before demonetization, UPI saw ~100k txn/month. UPI is at ~170 Mn Txns in Feb and ~3 Bn $ More transactions on UPI in 18 months than on Credit Cards in 18 years!

- 20. ACQUIRING BANK PARTNERS CONSUMER MOBILE ECOSYSTEM UPI SWITCH Bank 1 Bank 2 Bank 3 Bank 4 Bank N Network of 65 Issuer Banks WIDE MERCHANT ECOSYSTEM The BHIM UPI Ecosystem

- 21. A vision for a Good & Simple Tax! A single tax regime, across state borders Input Credit driven by buyer acceptance Powered by an API based platform-Goods & Services Tax Network (GSTN) Source: GSTN website GSTN enrolled 10 Million businesses, and has already collected $50 Bn in taxes in 6 months Nandan Nilekani, 2018

- 22. India has a unique digital Infrastructure A set of serendipitously developed open APIs, built as public good 2 31 64 7 eSign UPI BHIM GSTNAadhaar Auth FastTag ETC 8 Bharat Bill Pay (BBPS) 5 eKYC Digi- Locker

- 23. India will go from data poor to data rich in 3 years Digital Identity Paperless Process Commerce Payment Social Machine Learning & Algorithms We need to think about how this data wealth will translate to real wealth for users Nandan Nilekani, 2018 23

- 24. Elite & Affluent (37M HHs, 9%) $18.5k-$37k annual gross HH income Top 6-10% of highest income HHs Aspires (66M HHs, 23%) $7.4k-18.5k annual gross HH income Middle Class- Looking to trade up & aspire to upgrade (Disposable Income - 60%) Next Billion (103M HHs, 500m, 36%) $3.3k-$7.4k annual gross HH income New Consumers- HHs have some disposable income (33%), total spend $1 T Strugglers (80M HHs, 28%) <$3.3k annual gross HH income HHs with the majority of spend on basic needs such as food, shelter, power & water India-1 Process Reinvention India-2 Unlock Bharat India-3 Reduce Benefits Leakage Changing India How India will rise out of poverty over the next 20 years!

- 25. Unlocking India through India Stack India Stack Technology backbone for presence-less, paperless and cashless economy Financial Inclusion Payments, Lending, Savings 2nd Derivatives Healthcare Inclusion Primary Education Micro-business Expansion . . . Bringing economic mobility to the country

- 26. “ Data is empowering when it is in the hands of the people. We must invert the data, thus ensuring freedom and choice. This is Data Democracy

- 27. Lack of credit is due to lack of Data Nandan Nilekani, 2018 Bottleneck of lending is trust Knowledge asymmetry creates usurious money lenders Data measures capacity and intent to pay back a loan Ramesh (Engineer) Earns Rs 20,000 p.m. Mohan (Shopkeeper) Earns Rs 20,000 p.m. 0 10 10 0 0 1 1 1 0 1 0 0 0 0 1 1 1 1 0 0 0 0 1 00 0 01 1 1 10 0 0

- 28. India is pioneering Electronic Consent to unlock Data 28 Consent Collector Data Producers Data Consumers Consent Flow Data Flow Consent Artefact Lendr Money Flow

- 29. Millions of Borrowers Data Driven Algorithm Driven Consented Data Sharing Enabled by Mobile Electronic Contracts Digital Payments Credit Marketplaces Thousands of Lenders Digital Footprints Credit at scale can unlock the Indian Economy Nandan Nilekani, 2018